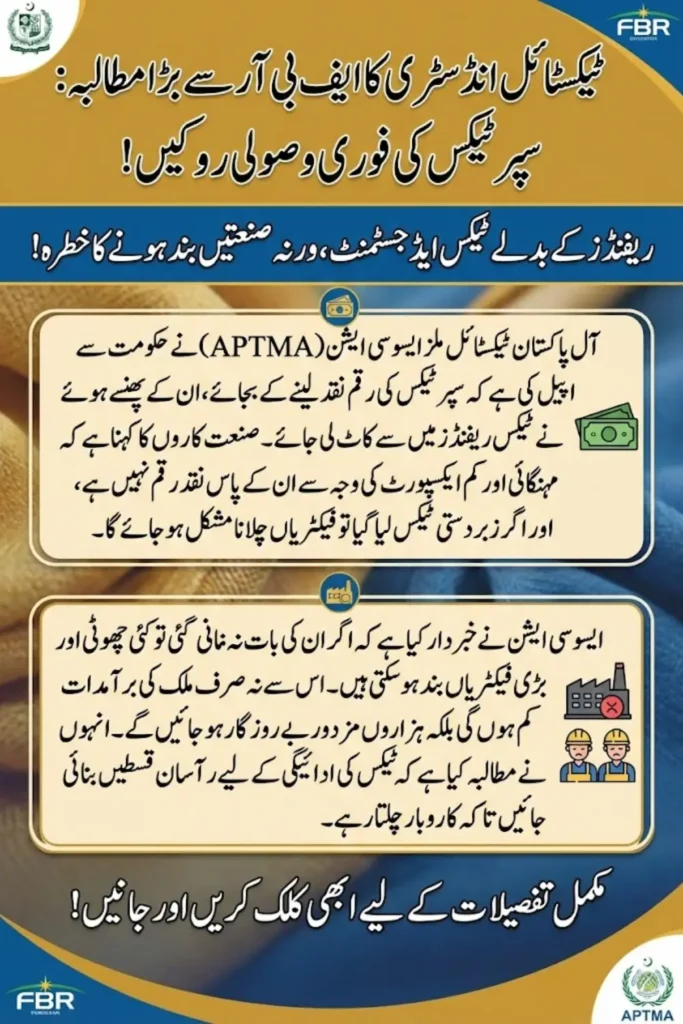

APTMA Urges FBR to Adjust Super Tax Against Pending Refunds

The All Pakistan Textile Mills Association has called on the Federal Board of Revenue to adjust Super Tax liabilities against long-pending tax refunds instead of enforcing immediate recovery. APTMA has warned that upfront collection of Super Tax could severely disrupt industrial operations and export activities, particularly in the already strained textile sector.

The association stated that manufacturers and exporters are currently facing serious liquidity challenges. Paying large Super Tax amounts in a single tranche would place excessive pressure on working capital and weaken the sector’s ability to function smoothly.

- APTMA appeals for adjustment instead of cash recovery

- Warning of operational and export disruption

- Focus on liquidity stress in the textile industry

You Can Also Read: BISP 8171 Wallet Account SIM 2026 – Complete Guide to Get and Activate Your Free SIM

Liquidity Pressure on Manufacturers and Exporters

APTMA highlighted that the textile sector is under acute financial pressure due to weak export orders and an unfavorable business environment. According to the association, exporters are not in a position to arrange large sums immediately without harming routine business operations.

The chairman of APTMA, Kamran Arshad, emphasized that demanding Super Tax payments upfront would drain working capital. This would affect daily operations such as procurement, production cycles, and order fulfillment, ultimately weakening export performance.

- Weak export demand affecting cash inflows

- Limited capacity to pay large taxes at once

- Risk to day-to-day business continuity

You Can Also Read: Ehsaas Program Registration 8171 2026 – Complete NADRA Guide for Beneficiaries

Economic Challenges Facing the Textile Sector

The textile industry is already dealing with multiple economic pressures that have reduced its resilience. High energy prices have increased production costs, while double-digit interest rates have made financing more expensive for businesses.

In addition to this, excessive taxation and rising imports of raw materials and intermediate goods have further weakened domestic manufacturers. APTMA warned that immediate recovery of Super Tax worth hundreds of billions of rupees would severely disturb cash flows.

- High energy tariffs increasing costs

- Expensive financing due to high interest rates

- Rising raw material and intermediate imports

You Can Also Read: BISP 8171 New Card Launch 2026 – Complete Guide to Apply

Impact of Immediate Super Tax Recovery

According to APTMA, enforcing immediate Super Tax recovery would make it difficult for businesses to meet basic financial obligations. These include salary payments, utility bills, and settlements with suppliers, all of which are critical for operational stability.

The association cautioned that such pressure could push many firms toward financial distress. Smaller and medium-sized enterprises, which have limited buffers, would be particularly vulnerable to abrupt tax recovery measures.

- Risk to salary and utility payments

- Pressure on supplier settlements

- Higher risk for SMEs

You Can Also Read: BISP 8171 Phase 3: Complete District List, Eligibility Criteria & Wallet Payment Guide 2026

APTMA Proposal for Super Tax Adjustment

APTMA proposed that Super Tax dues should be adjusted against pending refund claims instead of being recovered in cash. These refunds include income tax, sales tax, Technology Upgradation Fund, and Duty Drawback of Local Taxes and Levies.

The association further suggested that if any liability remains after adjustment, it should be converted into business-friendly installments. Spreading payments over a reasonable period would reduce financial stress and allow businesses to continue operations.

| Proposed Measure | Details |

|---|---|

| Refund Adjustment | Income tax, sales tax, TUF, DLTL |

| Remaining Liability | Convert into installments |

| Payment Approach | Gradual and business-friendly |

Concerns Over Super Tax Calculation Under Section 4C

APTMA also raised objections regarding the calculation of Super Tax for exporters under Section 4C. The association noted that exporters remained under the Final Tax Regime until tax year 2024, which affects how taxable income should be determined.

According to APTMA, Super Tax should be calculated on imputable income derived through reverse calculation of tax already paid. Without this approach, exporters may face unfair tax assessments and legal uncertainty.

- Exporters under Final Tax Regime until 2024

- Demand for reverse income calculation

- Risk of incorrect tax assessments

You Can Also Read: CM Punjab Laptop Scheme 2026 Complete Guide for Students Registration and Benefits

Need for Clear Guidelines and Stakeholder Engagement

The association expressed concern over the absence of clear guidelines from the tax authority. This lack of clarity has created uncertainty and opened the door to multiple interpretations of Super Tax rules.

APTMA urged FBR to engage with industry stakeholders and issue a generic clarification. Clear guidance would help avoid disputes, ensure fair application of the law, and improve compliance across the sector.

- Unclear rules creating uncertainty

- Risk of disputes and litigation

- Call for stakeholder consultation

You Can Also Read: CM Punjab E-Taxi Scheme 2026, Enroll Online and Required Documents

Demand to Suspend Recovery Proceedings

APTMA demanded that Super Tax recovery proceedings be suspended until the identified issues are resolved. The association believes enforcement without clarity would unfairly burden exporters and manufacturers.

Suspending recovery, according to APTMA, would provide temporary relief and allow time for a mutually acceptable solution that supports both revenue collection and industrial sustainability.

- Request for temporary suspension

- Relief for exporters and manufacturers

- Time for policy resolution

You Can Also Read: BISP 8171 Digital Wallet Payment Method 2026 – Easy Steps to Get Money via Easypaisa and JazzCash

Warning of Industry-Wide Consequences

The association warned that failure to provide workable relief could lead to widespread closures of textile units. Small and medium enterprises would be the first to shut down, followed by larger manufacturers if pressures persist.

APTMA cautioned that such closures would reduce exports, shrink the tax base, and lead to large-scale unemployment. Hundreds of thousands of workers could lose their jobs, creating broader economic and social challenges.

| Potential Impact | Expected Outcome |

|---|---|

| Factory Closures | Reduced industrial output |

| Exports | Significant decline |

| Employment | Large-scale job losses |

Conclusion

APTMA’s appeal highlights the fragile state of Pakistan’s textile sector amid rising costs and weak demand. Immediate Super Tax recovery, without adjustments or clarity, could destabilize an industry that is vital for exports and employment.

By adjusting Super Tax against pending refunds, clarifying calculation methods, and allowing installment-based payments, the tax authority can protect industrial activity while ensuring long-term revenue stability.

You Can Also Read: Punjab Government Rolls Out Digital Payment Cards for Imams Wazaif January 2026

FAQs

What is APTMA requesting from FBR regarding Super Tax?

APTMA has asked FBR to adjust Super Tax liabilities against pending tax refunds instead of enforcing immediate cash recovery.

Why does APTMA oppose upfront Super Tax payments?

The association says upfront payments would drain working capital and disrupt daily business operations.

What refunds does APTMA want adjusted against Super Tax?

APTMA wants adjustment against income tax, sales tax, TUF, and DLTL refunds.

What could happen if relief is not provided?

APTMA warns of factory closures, reduced exports, and large-scale unemployment in the textile sector.

You Can Also Read: Benazir Income Support Programme 2026